Finding, and keeping, hygienists and assistants is harder than ever. Rising wages and glossy DSO benefits can make your practice look bare-bones, but a retirement plan turns that liability into a hiring edge.

Clock’s ticking. From 2025, SECURE 2.0 makes auto-enrollment standard for most new 401(k)s, and many states already require a plan or a state auto-IRA. Miss the deadline and you risk fines, or watch talent leave.

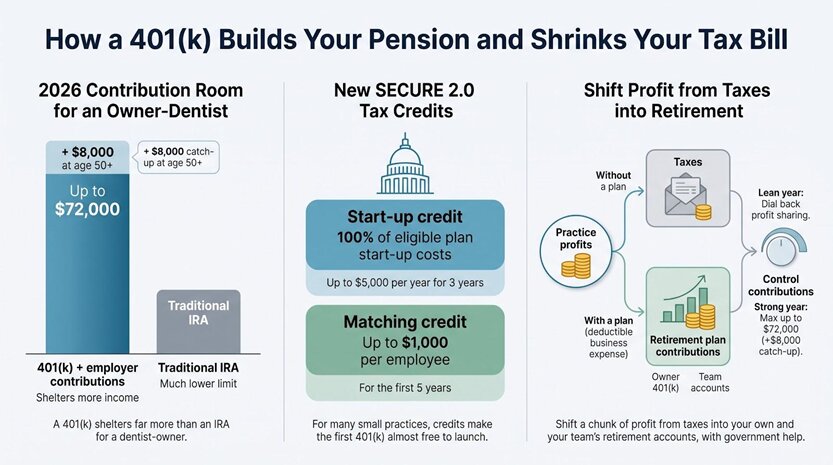

Done right, you can move up to $72,000 of 2026 income into tax-deferred savings and use fresh credits to offset most start-up costs. This guide compares every option, exposes real fees, and flags compliance traps.

Why offer a retirement plan in your dental practice

1. Win the talent battle.

Every week, new openings for hygienists and assistants flood job boards. Corporate chains lure candidates with glossy benefit packages that promise long-term security, not just a paycheck.

When your ad lists “competitive pay” but skips a 401(k), applicants notice. They picture working for decades with nothing set aside and keep scrolling. By contrast, a clear retirement benefit stops that scroll and says, “We invest in your future the way we invest in patient care.

Inside the office, the effect is just as powerful. Team members who see employer contributions land in their accounts feel valued. Turnover drops, gossip about better offers fades, and energy in the operatory lifts. Employees who believe they are building wealth alongside you stay longer, recommend friends, and treat patients like family, because they plan to be around to see those families return.

Offer a plan, and you shift the conversation from “What are you paying me today?” to “How can we grow together for years?” That is a competitive edge money alone cannot buy.

2. Build your own pension and shrink your tax bill.

No one hands a practice owner a pension at the end of a long career. If we want lifetime income, we have to create it ourselves. A retirement plan turns practice profits into a personal nest egg, sheltered from taxes until you need it.

Take the 2026 limits: combine your salary deferral, the employer match, and optional profit sharing, and you can move up to $72,000 out of today’s taxable income and into tomorrow’s retirement account. If you are fifty or older, tack on another $8,000 catch-up. That is real compounding power; far more than any IRA allows.

Better yet, every dollar you contribute for employees is a deductible business expense. Shift money you would have paid in taxes into staff accounts instead, and the IRS subsidizes your benefit program.

Congress sweetened the pot even more. Under SECURE 2.0, practices with fifty or fewer employees can claim a tax credit covering 100 percent of plan start-up costs (up to $5,000 per year for three years) plus up to $1,000 per employee in matching credits for five years. In many offices, that makes the first 401(k) almost free to launch and surprisingly cheap to fund.

Think of it this way: you can either write a big quarterly check to the Treasury or reroute a chunk of that money into your own retirement while giving staff a tangible reason to stay. The government is literally paying you to do the latter.

When profits surge, crank contributions up to the limit and boost your balance. Hit a lean year? Dial back optional profit sharing and preserve cash. With the right plan design, you control the throttle while staying in the good graces of the IRS.

In short, a retirement plan is not just a perk for employees; it is the most efficient wealth-building tool a dentist-owner has.

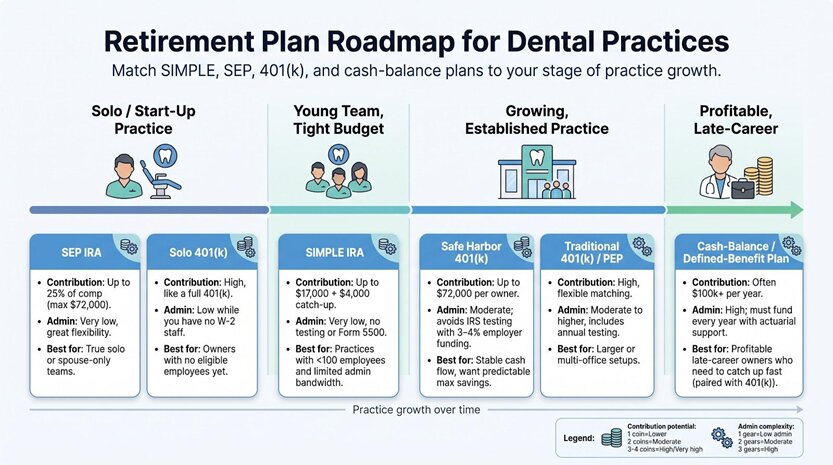

Retirement plan options for dental offices

Picking the right plan starts with knowing what is on the menu. We will walk through each option one at a time, beginning with the workhorse of small-business retirement planning: the 401(k).

1. 401(k) plans: the workhorse.

At its core, a 401(k) lets employees divert part of their paycheck into a tax-deferred account while you decide how generous to be with matching dollars. For 2026 the combined employee-plus-employer cap is $72,000, so this single vehicle can shelter serious money for an owner-dentist.

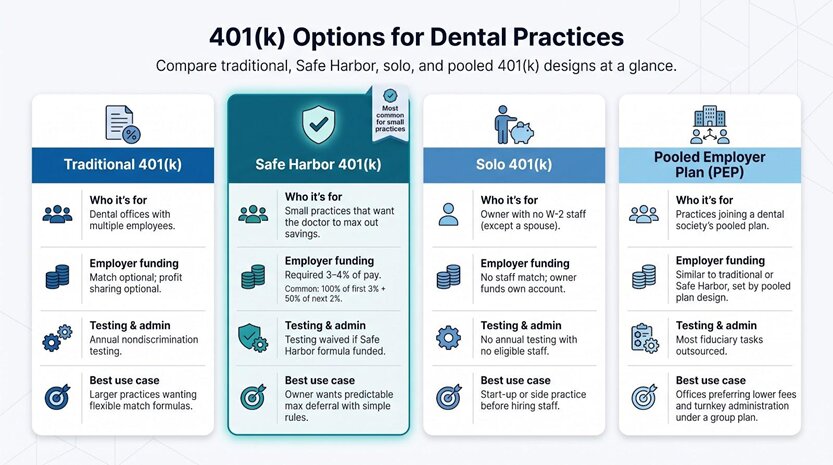

Traditional 401(k)

In the standard setup, staff choose whether to contribute. You may add a match or year-end profit share, but you are not required to. The trade-off is testing. If too few employees join, the IRS limits how much highly compensated people (you) can defer.

Safe Harbor 401(k)

Safe Harbor skips that headache. Promise either a match of up to four percent of pay or a flat three-percent contribution to everyone, and the compliance tests disappear. Most small practices adopt this design because it guarantees the doctor can max out while keeping admin simple.

Industry surveys show that almost 92 percent of employers with a plan already budget for a match, and the most common Safe Harbor formula, 100 percent of the first 3 percent of pay plus 50 percent of the next 2 percent, keeps total employer cost right at the four-percent threshold that waives IRS testing.

Solo 401(k)

Running a start-up practice with no W-2 staff besides a spouse? A Solo 401(k) gives you the same high limits without any matches, notices, or annual testing. Remember: the day you hire an eligible employee, the plan must convert to a regular 401(k) and all the rules apply.

Pooled employer plans (PEPs)

Some state dental societies now sponsor pooled 401(k)s. You join their umbrella plan, share costs with dozens of other offices, and outsource virtually all fiduciary tasks. Fees are often lower than a standalone micro-plan, though you give up a bit of design flexibility.

Bottom line: if consistent cash flow and owner savings are priorities, a well-built 401(k), especially the Safe Harbor flavor, delivers unmatched contribution limits, tax benefits, and recruiting punch. The next sections explore simpler (and more advanced) alternatives so you can match the plan to your stage of practice growth.

2. SIMPLE IRA: the starter kit.

Picture a retirement plan you can set up before lunch, explain in one staff meeting, and run for pennies a day. That is the appeal of the SIMPLE IRA, designed for businesses with 100 or fewer employees, which fits nearly every private practice.

Employees decide how much to save, up to $17,000 in 2026, plus a $4,000 catch-up once they hit fifty. Your part is simple: either match their savings dollar-for-dollar up to three percent of pay or drop a flat two-percent contribution into every eligible employee’s account. No annual testing, no Form 5500, no outside auditor. The custodian handles paperwork while you handle crowns.

For a young practice still smoothing cash flow, that low-lift structure is gold. You offer a real benefit, grab a tax deduction on the match, and avoid the administrative mountain a 401(k) brings.

There is a ceiling, though. Because contribution limits sit well below a 401(k), owner-dentists often outgrow the SIMPLE once profits climb. Thanks to new rules, you can now switch to a Safe Harbor 401(k) mid-year instead of waiting until January. Many offices make that leap as soon as the doctor is ready to save more than the SIMPLE allows.

In short, use the SIMPLE IRA when budget or bandwidth is tight, then trade up when you are ready for bigger tax savings.

3. SEP IRA: flexibility for solo or micro practices.

Think of a SEP IRA as the owner’s choice plan. You decide whether to put in money each year and how much, from zero all the way up to 25 percent of compensation, capped at $72,000 for 2026. No employee deferrals, no match formulas, and practically no paperwork.

That freedom is a lifesaver in an early acquisition year or after an unexpected equipment purchase. Skip contributions one season, catch up the next, no questions asked. The entire deposit is a business deduction, and accounts live at any brokerage you like.

The rub shows up when you have staff. Whatever percentage you give yourself, you must give every eligible employee the exact same slice of their pay. Great if you employ only a spouse or one long-tenured assistant. Painful if six part-timers suddenly qualify. Because workers cannot add their own dollars, some view the SEP as less valuable than a 401(k) match, dulling its retention punch.

For a true solo dentist or two-person family practice, though, a SEP trades a stack of rules for a single page of instructions and the chance to load tens of thousands into retirement when profits surge. It shines as a transitional tool: quick to open, easy to fund, and just as easy to replace with a Safe Harbor 401(k) once the team and payroll grow.

4. Defined-benefit and cash-balance plans: extra power for late-career saving.

Some dentists wake up at fifty-five, practice humming, loans gone, and realize they are behind on retirement. A 401(k) alone will not close that gap fast enough. Enter the defined-benefit family of plans, especially the modern cash-balance design.

Think of a cash-balance plan as a personal pension you control. Each year an actuary sets a required contribution large enough to fund a promised future benefit. Because the target is high and the owner is older, the math often allows six-figure deposits, sometimes north of $200,000 a year, deductible to the practice and growing tax-deferred.

Pair that with your existing Safe Harbor 401(k) and you can sock away more than a quarter-million dollars annually, all before the IRS takes its cut. For a profitable, mature practice, the tax savings alone can cover a chunk of the staff funding that federal rules require.

The commitment is real. Once established, the plan must be funded every year until it is formally terminated, usually five years or more. You also pay for annual actuarial valuations and federal filings. But for many late-career owners, the ability to compress two decades of saving into one brisk sprint outweighs the complexity.

In short, a cash-balance plan is the nitrous button of retirement planning: unnecessary early in your career, invaluable when you need maximum acceleration toward the finish line.

Costs and contributions: what to expect

Understanding the cost components.

The price tag on a retirement plan comes in two parts: the visible checks you write each year and the hidden nicks buried in investment expenses. As outlined on this 401k planning page, one ongoing-management approach benchmarks plan expenses on a regular cycle, comparing administration, employer funding, and investment costs against efficiency targets so you can see where your own numbers stand against peer practices. We will start with the visible ones.

Plan administration is the invoice you pay to keep the engine running. Recordkeepers track balances, a third-party administrator files forms, and an advisor steers investments. For a plan with roughly five million dollars inside, the 2025 401(k) Averages Book pegs total fees near 1.08 percent of assets (about fifty-four thousand dollars a year). A fifty-million-dollar plan, by contrast, averages just 0.76 percent. The smaller the plan, the bigger the percentage bite.

Next comes employer money flowing into participant accounts. In a Safe Harbor 401(k) that is typically three or four percent of payroll. A SIMPLE IRA locks you into either a three-percent match or a two-percent all-employee contribution. A SEP takes whatever slice you choose but forces you to share that same slice with every eligible worker. These dollars feel like an expense today, yet each one is a deductible business cost and an investment in staff loyalty.

Finally, watch for embedded costs inside mutual funds or collective trusts. Revenue-sharing, wrap fees, and 12b-1 charges often hide here, eroding net returns while staying invisible on the surface statement. Regulators require providers to disclose these numbers, but you have to ask, then compare them with low-cost index options to know whether the premium is justified.

Add those three elements together: admin invoices, employer contributions, and fund expenses, and you have the all-in cost of your plan.

Conclusion

A retirement plan is a numbers problem with a people payoff. Pick the structure that matches your practice's size and cash flow (SIMPLE, SEP, Safe Harbor 401(k), or cash-balance) and benchmark the three cost buckets, admin, employer contributions, and fund expenses, at least once a year. Get that right, and the same plan that satisfies SECURE 2.0 also becomes the reason a great hygienist chooses your chair over the DSO down the street.