Two common responses commercial property/dental practice owners make when asked if cost segregation was applied to their properties are, “what is cost segregation?” and, “wouldn’t my CPA handle this?” For this reason I will briefly discuss cost segregation, describe why it is important, and finally the impetus behind the “CPA” puzzle.

Cost Segregation is a tax saving strategy which allows commercial property owners an opportunity to significantly increase their cash-flows by accelerating tax deductions on specific building costs. The basic difference between cost segregation and traditional straight-line depreciation is time value of money. Ultimately both scenarios end up with the same amount of depreciation deductions, but with the straight-line method you are effectively overpaying taxes on the front. By accelerating depreciation through cost segregation, the money otherwise paid in tax may be retained, used to pay down debt, or invested in other assets.

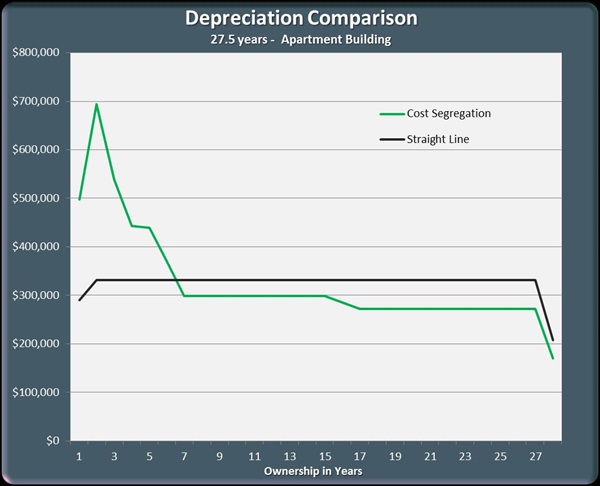

Figure 1. Compares tax deductions using the two methods. With cost segregation you have more deductions earlier, lowering current tax obligations, thus increasing available cash.

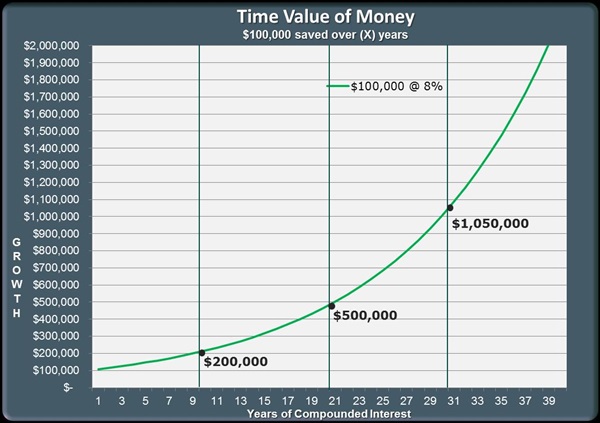

Let’s say you have the option to take a $100,000 cash payment today, or the same amount paid in equal installments over the next 39 years. Which would you prefer? Taking it a step further, consider the earning potential of the lump sum payout invested at reasonable rate of return (or in your business) over the same period. Your decision should be simple.

Figure 2. Illustrates the time value of money and compounded growth should you invest $100,000 at a reasonable 8% interest rate. Note the value doubles every ten years.

Now, to the CPA confusion. Since accountants are inherently associated with all things tax, it stands to reason why the aforementioned CPA question occurs. Nonetheless, CPAs do not perform cost segregation studies because they generally do not have the specialized expertise to do so. According to the IRS “reliable” cost segregation studies are those conducted by “qualified” professional firms competent in design, construction, auditing, and estimating procedures relating to building construction. Therefore, studies conducted by specialized engineering firms are more reliable than studies by those without construction cost backgrounds. Ultimately, if someone did not physically visit and document your property, a complete cost segregation study was not applied. It is entirely possible that your tax professional may have identified a couple items and placed them into the appropriate 5 or 7 year depreciation schedules, but this is far from complete. Alternatively, they may have partnered with qualified engineer-based cost segregation firm to conduct a complete study. As a business owner it is in your best interest to know the difference as the cash equivalent value of your tax saving benefit can be between 5-10% of the structural value. That’s correct, $50K-$100K per $1M in structural value.

Yes, most tax professionals are aware of cost segregation, and according to the Journal of Accountancy should recommend the use of cost segregation to their clients. This does not however mean they bring it up during the busy tax season, or have a qualified partner to conduct the study. Either way, businesses can partner directly with a cost segregation firm to perform studies on their behalf - providing the required documentation their tax professionals need. Furthermore top cost segregation firms should offer a no cost analysis for your specific property or properties. Once you see an estimate of your numbers you can then make an informed decision on whether applying a complete study would be economically feasible. Again, your decision should be simple.

For 2017 tax year updates See Post: Provisions of the Tax Cuts and Jobs Act That Affect Building Owners

Sources:

1. AICPA : Journal of Accountancy, Aug 2004, Cost Segregation Applied

2. IRS: Cost Segregation Audit Techniques Guide, Ch. 3 Cost Segregation Approaches, Update 2016